CBAM will add approximately €70-€100 per tonne of embedded CO₂ to the cost of importing South African aluminium into the EU. Because SA’s coal-powered smelters produce up to 18 tonnes of CO₂ per tonne of aluminium – nearly three times the EU average of 6.6 tCO₂e/t – exporters face significantly higher carbon surcharges than competitors using cleaner energy. However, recycled aluminium produces just 0.52 tCO₂e per tonne, representing a 95% reduction that directly translates to lower CBAM costs. For SA businesses in the aluminium value chain, this creates both a serious threat and a practical opportunity – one that starts at scrap yards near me.

What Is CBAM and Why Does It Matter for South Africa?

CBAM is the EU’s carbon border tax – a mechanism that requires European importers to purchase certificates for the carbon emissions embedded in goods like aluminium, steel, cement, fertilisers, electricity, and hydrogen. For South Africa, one of the most carbon-intensive aluminium producers in the world, CBAM represents a direct cost threat to €1.1 billion worth of exports.

The mechanism entered its definitive phase on 1 January 2026, following a two-year transitional period during which EU importers were required to report emissions data without paying carbon costs. Now, the financial obligation has begun. EU importers must buy CBAM certificates priced in line with the EU Emissions Trading System (EU ETS) – currently around €70-€100 per tonne of CO₂. The ETS is the EU’s cap-and-trade system that sets a price on carbon emissions from large industrial installations across Europe.

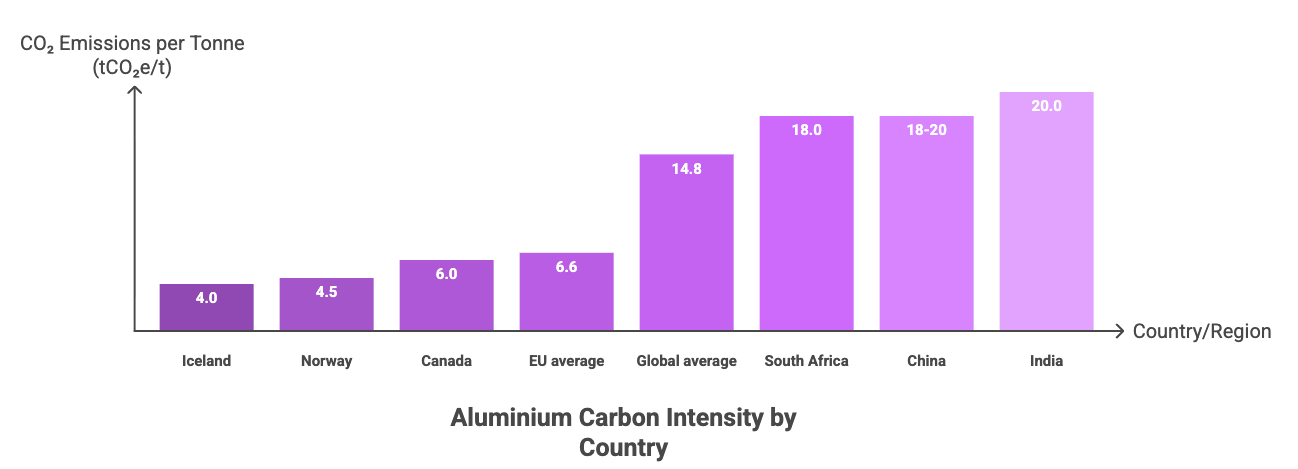

South Africa is particularly exposed because roughly 80% of the country’s electricity comes from Eskom’s coal-fired power stations. Aluminium smelting is extraordinarily energy-intensive, and when that energy comes from coal, the resulting carbon footprint dwarfs that of competitors using hydropower or renewables. Hillside Aluminium in Richards Bay, SA’s largest smelter, produces aluminium with a carbon intensity of approximately 18 tCO₂e per tonne (tCO₂e stands for tonnes of carbon dioxide equivalent – a standard measure of greenhouse gas emissions). Compare that to the EU average of just 6.6 tCO₂e/t, largely thanks to hydroelectric and nuclear power, and the scale of SA’s challenge becomes clear.

According to the Carbon Trust, approximately 25% of South Africa’s aluminium exports and 16% of iron and steel exports go to the EU, placing these sectors firmly in CBAM’s crosshairs. The African Climate Foundation and LSE estimate that CBAM could reduce African aluminium exports to the EU by up to 13.9%. For a country that relies on these industries for jobs and foreign currency, the stakes could not be higher.

| Aluminium Source | tCO₂e per Tonne | CBAM Cost Indicator (at €85/tCO₂) |

|---|---|---|

| South Africa – coal-powered (Hillside Aluminium) | ~18.0 | ~€1,530/t – Extreme exposure |

| Global average – primary aluminium | ~15.1 | ~€1,284/t – Very high exposure |

| EU average – hydro/nuclear powered | ~6.6 | ~€561/t – Moderate (offset by ETS) |

| Recycled aluminium | ~0.52 | ~€44/t – Minimal exposure |

Sources: International Aluminium Institute; Anthesis Group SA analysis. CBAM cost estimates assume €85/tCO₂ and exclude free allowance adjustments.

How Much of South Africa’s Aluminium Export Value Is at Risk Under CBAM in 2026?

In 2023, South Africa’s CBAM-covered exports to the EU were valued at €1.1 billion, accounting for 5% of the country’s total exports. While CBAM costs in 2026 remain relatively modest thanks to remaining free allowances (temporary exemptions being phased out under the ETS), they escalate sharply each year – and by 2034, when free allowances reach zero, CBAM levies could exceed 50% of SA aluminium export value without meaningful decarbonisation.

South Africa produces approximately 700,000 tonnes of primary aluminium annually – roughly 1% of global output – making it the 8th largest aluminium exporter to the EU. The sector is a significant employer, supporting around 11,000 direct jobs and an estimated 29,000 indirect positions across the value chain. Total SA aluminium exports were worth approximately $2.25 billion in 2023, and the EU remains one of the most important destination markets.

One critical factor amplifies SA’s vulnerability: the gap between South Africa’s domestic carbon tax and the EU carbon price. SA’s carbon tax sits at approximately R190 per tonne of CO₂ (under $20/t) – a fraction of the EU ETS price of €70-€100/tCO₂. Under CBAM rules, the carbon price already paid in the country of origin can be deducted from the CBAM certificate obligation. But the difference between SA’s carbon tax and the EU price is so large that this deduction provides only marginal relief.

Hulamin, a major South African aluminium manufacturer, has publicly warned that CBAM levies could eventually strip more than half the value from SA’s aluminium exports to Europe. The escalation timeline below illustrates how the financial pressure builds as free allowances disappear.

| Year | Free Allowances Remaining | Estimated CBAM Cost Impact on SA Aluminium | Risk Level |

|---|---|---|---|

| 2026 | ~97.5% | Low – limited certificate purchases required | Low |

| 2028 | ~80% | Growing – meaningful cost pressure begins; downstream products added to CBAM scope | Medium |

| 2030 | ~50% | Significant – carbon costs become material to export margins | High |

| 2032 | ~25% | Severe – exporters without low-carbon strategies face margin erosion | High |

| 2034 | 0% | Full CBAM cost – could exceed 50% of SA aluminium export value | Critical |

Sources: EU Commission CBAM implementation package (December 2025); Anthesis Group SA sector analysis; Argus Media. Free allowance phase-out schedule is indicative based on current EU ETS reform trajectory.

South Africa’s Aluminium Export Exposure at a Glance

| Metric | Figure |

|---|---|

| CBAM-covered exports to EU (2023) | €1.1 billion |

| Share of SA exports affected by CBAM | ~5% of total exports |

| SA aluminium exports to EU | ~25% of total aluminium exports |

| Annual primary aluminium production | ~700,000 tonnes |

| SA ranking as EU aluminium supplier | 8th largest |

| Direct jobs in SA aluminium sector | ~11,000 |

| Indirect jobs across value chain | ~29,000 |

| SA carbon intensity (coal-powered) | ~18 tCO₂e/t |

| SA domestic carbon tax | ~R190/tCO₂ (under $20) |

| EU ETS carbon price | €70-€100/tCO₂ |

Can South African Exporters Lower CBAM Costs by Using More Recycled Scrap Metal?

Yes – and by a dramatic margin. Recycled aluminium produces approximately 0.52 tCO₂e per tonne, compared to 15-18 tCO₂e for primary aluminium from coal-powered smelters. That is a 95% reduction in embedded carbon, which translates directly to 95% fewer CBAM certificates required by EU importers. For manufacturers and exporters looking for a practical, immediate way to reduce their CBAM exposure, increasing recycled content is the single most effective lever available.

The mechanics are straightforward. Under CBAM, EU importers pay based on the embedded emissions – known as Scope 1 (direct emissions from production) and Scope 2 (emissions from purchased electricity) – in the goods they bring into Europe. Lower embedded emissions mean fewer certificates to buy, which means lower costs. Products manufactured with a higher proportion of recycled aluminium carry a fraction of the carbon footprint of those made from virgin metal, making them significantly more price-competitive in CBAM-regulated markets.

According to the International Aluminium Institute, recycling aluminium saves 95% of the energy required for primary production – and a comparable percentage in greenhouse gas emissions. Post-consumer aluminium scrap carries an embedded carbon footprint of roughly 0.5 tCO₂e regardless of how the original metal was produced. This means even aluminium that was initially smelted using coal-heavy electricity effectively “resets” its carbon profile when it enters the recycling stream.

For South African fabricators, foundries, and exporters, the implication is clear: working with quality scrap metal suppliers who can deliver clean, well-sorted aluminium scrap is no longer just good business practice – it is a competitive necessity. Companies that increase their recycled aluminium content position themselves and their EU customers with measurably lower CBAM costs. If you are looking to understand how to get the best value from non-ferrous metals in this new environment, our guide on best practices for selling copper, aluminium and brass is a practical starting point.

How Could CBAM Increase Demand and Prices for Clean, Well-Sorted Aluminium Scrap in South Africa?

CBAM creates a premium market for low-carbon inputs, which means clean, properly sorted aluminium scrap is set to become more valuable than ever. As EU importers seek to minimise their CBAM certificate costs, demand for recycled aluminium inputs will rise – and that demand flows directly back to local scrap generators, collectors, and recyclers across South Africa.

Not all scrap is created equal in a CBAM context. Clean, alloy-sorted aluminium scrap that can be recycled with minimal additional processing carries the lowest embedded carbon footprint. Contaminated or mixed loads, on the other hand, require more energy-intensive sorting and remelting, which increases emissions and erodes the CBAM advantage. This is why “scrap quality” matters more now than it ever has before.

For smaller businesses, workshops, construction firms, and demolition contractors who generate aluminium scrap, CBAM creates an indirect but real benefit. Higher demand for quality scrap from manufacturers seeking to reduce their carbon exposure is likely to drive premium pricing for properly prepared material. Businesses that invest a small amount of effort in separating aluminium from other metals – and keeping different aluminium alloys apart – stand to earn significantly more per kilogram.

Here is what quality-conscious sorting looks like in practice. Keep aluminium separate from steel, copper, and other metals. Where possible, sort by alloy type – cast aluminium (such as engine blocks) versus wrought aluminium (such as window frames or sheet metal). Remove contaminants like plastic, rubber, paint, and oil. Store scrap in dry conditions to prevent corrosion. These steps are straightforward, but they make the difference between standard pricing and premium rates at scrap yards near me.

South Group Recycling operates across Johannesburg, Cape Town, Pretoria, and Durban, providing professional sorting, competitive pricing, and free collection for larger volumes. As CBAM reshapes the value of recycled materials, working with an experienced, licensed recycler ensures you capture the full market value of your scrap metal near me.

What Should South African Businesses Do Now to Prepare for CBAM?

Preparation is the difference between being caught off guard and turning CBAM into a competitive advantage. While the full financial impact will build gradually over the next eight years, the businesses that act now will be best positioned when costs peak.

The first priority is understanding your supply chain’s carbon footprint. Every business that manufactures, processes, or exports aluminium or steel products to the EU needs to know its Scope 1 and Scope 2 emissions. Scope 1 covers direct emissions from your own operations – fuel burned in furnaces, for instance. Scope 2 covers indirect emissions from the electricity you consume. In South Africa, Scope 2 is typically the dominant factor because of the coal-heavy Eskom grid. Getting accurate emissions data is the foundation of any CBAM strategy, and it is also what your EU customers will increasingly demand from you.

Next, look at increasing the recycled aluminium content in your production. As the data above demonstrates, the carbon difference between primary and recycled aluminium is enormous – 18 tCO₂e/t versus 0.52 tCO₂e/t. Even a modest increase in recycled input can meaningfully reduce the CBAM burden on your EU-bound products. Establishing reliable relationships with quality scrap metal suppliers is an essential step.

Documentation and traceability will also become critical. EU importers need to verify the embedded emissions in the products they purchase, and they will increasingly favour suppliers who can provide clear, auditable data on material origins and carbon intensity. Businesses that can demonstrate a verified low-carbon profile will have a tangible edge in retaining and winning EU contracts.

Finally, keep a close eye on South Africa’s own carbon tax trajectory. The SA government is under growing pressure to raise the domestic carbon price closer to international levels – both to retain carbon tax revenue that would otherwise flow to the EU through CBAM, and to support the country’s own climate commitments. Any increase in SA’s carbon tax would reduce the CBAM differential and lower the additional cost burden on exporters. Understanding how these two policies interact is important for long-term planning.

For a broader perspective on how recycling supports climate action in South Africa, our article on sustainable recycling practices explores the circular economy benefits beyond CBAM.

Partner with South Group Recycling

CBAM is changing the economics of aluminium in South Africa – and recycled scrap is at the centre of the solution. Whether you are a manufacturer looking to lower your carbon exposure, an exporter preparing for EU compliance, or a business with aluminium scrap to sell, South Group Recycling can help.

With over 10 years of experience, operations across 16 African countries, and facilities in Johannesburg, Cape Town, Pretoria, and Durban, we provide competitive pricing, professional sorting, and free collection for qualifying volumes. Contact us today to discuss how we can support your CBAM strategy.

Find your nearest scrap yard →

The Bottom Line: CBAM Is a Threat and an Opportunity

CBAM is not simply a cost to be absorbed – it is a structural shift that will reshape South Africa’s aluminium and scrap metal markets over the next decade. For businesses that rely on EU market access, the choice is between proactive adaptation and gradual erosion of competitiveness. The numbers are clear: coal-powered primary aluminium faces mounting carbon surcharges, while recycled aluminium offers a 95% reduction in embedded emissions and a direct path to lower CBAM costs.

For the scrap metal industry, CBAM represents a rare tailwind. Higher demand for quality recycled aluminium inputs, premium pricing for well-sorted material, and a strengthening link between recycling and climate action all point in the same direction: the value of doing recycling well is going up.

South Group Recycling has spent more than a decade building the infrastructure, expertise, and relationships to serve South Africa’s metals recycling market. As CBAM changes the rules, we are here to help businesses – from large exporters to local scrap generators – navigate this transition. Get in touch to find out how we can support your business.